Formulary Exception: How to Get a Non-Formulary Drug Covered

Your medication worked. Your doctor prescribed it. And now your insurance says it's not covered.

Learning that your insurance plan doesn't cover your treatment is frustrating, and often leaves folks with a lot of questions. Whether you got a letter in the mail or a message from your doctor's office, you're probably wondering – what in the world is a formulary, and what do I do if my drug isn't on it?

A formulary is the list of drugs that are covered by your insurance plan. But what most people don't know is that even if your treatment isn't on the list, you can still get covered. Most plans are required to maintain a formulary exception process, and if that's denied, you have the right to appeal.

And when a formulary exception is granted, it means your insurance has to cover your treatment again – even if it's not on their official list.

Let's break down what to do if your med is "not on formulary", and how to get it covered again.

How to get a non-formulary drug covered: Quick answer

To get a non-formulary drug covered, request a formulary exception from your plan. Start by confirming why you were denied: Check your plan's formulary and get the denial reason in writing. Then, submit the exception request to your insurance. Ask your doctor for a letter of medical necessity to support your request, and clearly document any failed alternatives or other reasons why you need the exception. If your exception is denied, you have the right to appeal – and appeals supported by strong clinical evidence, legal citations, and a clear patient narrative succeed far more often than most people realize.

What Is a Formulary – and What Does "Not on Formulary" Mean?

A formulary or drug list is your insurance plan's list of approved medications. It's organized into tiers – typically ranging from low-cost generics to high-cost specialty drugs – and it determines what your plan will cover and at what cost.

When your drug is "not on formulary," it means your plan has decided not to include it on that list. When it's "non-preferred," it means they'll technically cover it, but only after you've jumped through additional hoops (usually trying cheaper alternatives first).

Here's the part most people don't realize: formularies aren't just about if a medication works. They're heavily influenced by rebate deals between insurers, pharmacy benefit managers (PBMs), and drug manufacturers. A drug can be clinically effective, widely prescribed, and still get dropped from a formulary due to behind-the-scenes business deals. The medication didn't change. The science didn't change. But the business math did.

That distinction matters, because it means a formulary exclusion is often a financial decision dressed up as a medical policy – and financial decisions can be challenged.

How Formulary Denials Happen

If you're reading this, it's probably because you got a letter, a notification, or a phone call that tells you your medication isn't covered. These notifications can come in different forms, and what you should do next depends on what you're dealing with. Find the one below that sounds like you.

You got a letter saying your medication is being removed from formulary. This is a prospective formulary change – your plan is dropping the drug on a future date. Insurers are supposed to send this 60 days in advance (though the notice is mailed 60 days ahead, that doesn't mean it arrives that early). You only get this notice if the insurer knows you're currently filling the medication. If you just switched plans or are newly prescribed the drug, you won't be notified.

You got a denial notification in your pharmacy or insurance app. A short message in your CVS, Walgreens, or insurer app telling you the claim was denied. These notifications are a starting point, but they're often frustratingly incomplete – a brief description without the full denial reason, the policy they applied, or your appeal rights. Don't assume this is the whole story.

You got a formal denial letter in the mail. This is the letter with the specific denial reason and information about your rights. It's the most complete notification – but it can take two to four weeks to arrive after the initial denial. That's weeks you could be using to prepare.

Your doctor or pharmacist told you it's not covered. Sometimes your provider checks your benefits, sees the drug isn't on formulary, and tells you they're going to switch you to something else. In this scenario, you may not receive a formal denial at all. If this happens, it's worth having a conversation with your provider about whether you want to switch, because you do have other options.

Regardless of how you found out: call your insurer and request the full documentation – the exact denial reason, the coverage policy they applied, and your appeal rights and process. Ask them to send it the fastest way possible: through your online portal, faxed to your provider who can share it with you, or emailed directly. Don't wait for paperwork to arrive on its own timeline. And don't wait for the formal denial letter to start preparing – you can begin gathering documents and building your case as soon as you know there's a problem.

The Biggest Misconception: "Not Covered" Doesn't Mean Final

The most common reaction when patients hear "not on formulary" is to assume there's nothing they can do. That it's a final decision — and that "not covered" means "can never be covered."

It's not. And this is perhaps the single most important thing to understand about the entire process.

Even many providers will tell patients "it's not covered, there's nothing we can do" – and that's simply not accurate. You have a legal right to request a formulary exception, and if that's denied, you have additional appeal rights including independent external review. Insurance companies benefit enormously from people believing that "not covered" is the end of the road. For the vast majority of denial types, it's actually the beginning.

A note on weight loss medications: If your medication is excluded specifically because your plan doesn't cover drugs for weight loss as a category, that's a plan exclusion – which is different from a formulary exclusion and significantly harder to fight. If you're in this situation, we've got a whole guide to plan exclusions here.

Formulary Exception vs. Prior Authorization: What's The Difference?

In many cases, you can't formally request an exception until there's a written denial. The PA is often what generates that denial.

What Is a Prior Authorization (PA)?

A prior authorization is when your insurer requires your doctor to request approval before a medication will be covered. Your doctor submits clinical documentation, and the insurer decides whether the drug meets the plan's coverage criteria.

A medication can be on the formulary and still require a PA. Many plans apply PA requirements to brand-name, specialty, or high-cost drugs.

If a drug is non-formulary (not on the approved drug list), coverage usually requires an exception review — and in most plans, that request is submitted through the same PA system. That's why the terms often get confused.

What is a Formulary or Medical Exception?

A formulary exception is a formal request to cover a drug that is not included on your plan's formulary. You're asking the insurer to make an exception based on medical necessity, failure of covered alternatives, lack of equivalent options, or risk of harm from switching.

How the process actually works

In many cases, you can't formally request an exception until there's a written denial. The PA is often what generates that denial.

If your current medication is removed:

Benefits are checked → A PA is required or the drug is non-formulary → A PA is submitted → The PA is denied → You request a formulary exception and/or file an appeal

If you're prescribed a new non-formulary medication:

The prescription is sent to the pharmacy → You're told it's not covered or needs a PA → A PA is submitted → The PA is denied → You request a formulary exception and/or file an appeal

If you're forced to switch and the new medication isn't working:

Your insurer requires you to switch to a covered alternative → You try the new medication → It's ineffective, causes side effects, or worsens your condition → Your provider submits a PA to return to the original medication → The PA is denied → You request a formulary exception and/or file an appeal

Why this matters: In all three situations, the prior authorization often generates the written denial that unlocks your right to appeal.

Insurance rules are layered and technical. Claimable helps you move from denial to action — so treatment decisions stay where they belong: between you and your doctor.

How to Request a Formulary Exception

Make sure you have an active denial

Before you can pursue a formulary exception, you generally need a current, documented denial.

If you've received notice that your formulary is changing on a future date, don't wait and hope it resolves itself. Ask your provider to submit a new prior authorization on the first day the change takes effect. Once the change is active, any prior approval is typically no longer valid — even if it feels like it should be.

Your provider may not automatically resubmit a PA, but they can. Just ask.

Once that new PA is denied, you have a clean, current denial to challenge.

Choose your pathway

There are two ways to pursue a formulary exception, and you can actually do both at the same time:

The provider pathway: Your doctor submits a formulary or medical exception request to your insurer, focused on clinical justification. This may include documentation showing that covered alternatives were ineffective (therapeutic failure), alternatives caused adverse effects (intolerance), and/or alternatives are unsafe due to contraindications or FDA warnings. This pathway centers on proving medical necessity.

The patient appeal pathway: You submit a formal patient appeal directly to your health plan. This is the pathway you control immediately. It allows you to go beyond clinical arguments and include how the denial personally impacts your health, life and finances and call out specific legal protections and policy inconsistencies that show your care should be covered. You can also attach your provider's medical justification.

You don't have to choose just one. Pursuing both pathways can increase your chances — think of it as "more shots on goal." If you're already researching on your own, we recommend starting a patient appeal – it puts more tools at your disposal and doesn't depend on your provider's timeline or capacity. Appeals are strongest when patients and providers work together.

A note on "formulary exception forms"

If you've been searching for a standard "formulary exception form," you're not alone. Most exception forms are designed for providers, not patients. And even when they exist, they often don't leave room to fully present your case — including clinical evidence, legal arguments, and policy support.

Don't get stuck form-hunting. You can submit a formal appeal letter directly to your plan's appeals department — or use Claimable to generate and submit the request for you. If your insurer needs additional clinical documentation, they can request it directly from your provider during the review process.

Use the right language

Here's what most guides won't tell you: the specific language you use can determine whether your request is properly categorized or quietly buried. Insurers route requests based on trigger words. If you don't explicitly ask for a "formulary exception" and state why you qualify, your request may be miscategorized as a general inquiry – which means longer timelines, less scrutiny, or it simply being ignored.

You qualify for a formulary exception under three main categories:

- Therapeutic failure – the formulary alternatives were tried and either never worked or stopped working over time. Be specific: name each medication, how long you were on it, and what happened.

- Adverse events – you experienced side effects that made the formulary alternatives intolerable. This includes reactions that led to hospitalization, allergic responses, or side effects that significantly impacted your quality of life.

- Clinical contraindication – the formulary alternatives are medically inappropriate for you. This could be due to drug interactions, an FDA black box warning for your specific situation, or a co-existing condition that makes the alternative unsafe.

State your category clearly and explicitly in your request. Don't make them guess.

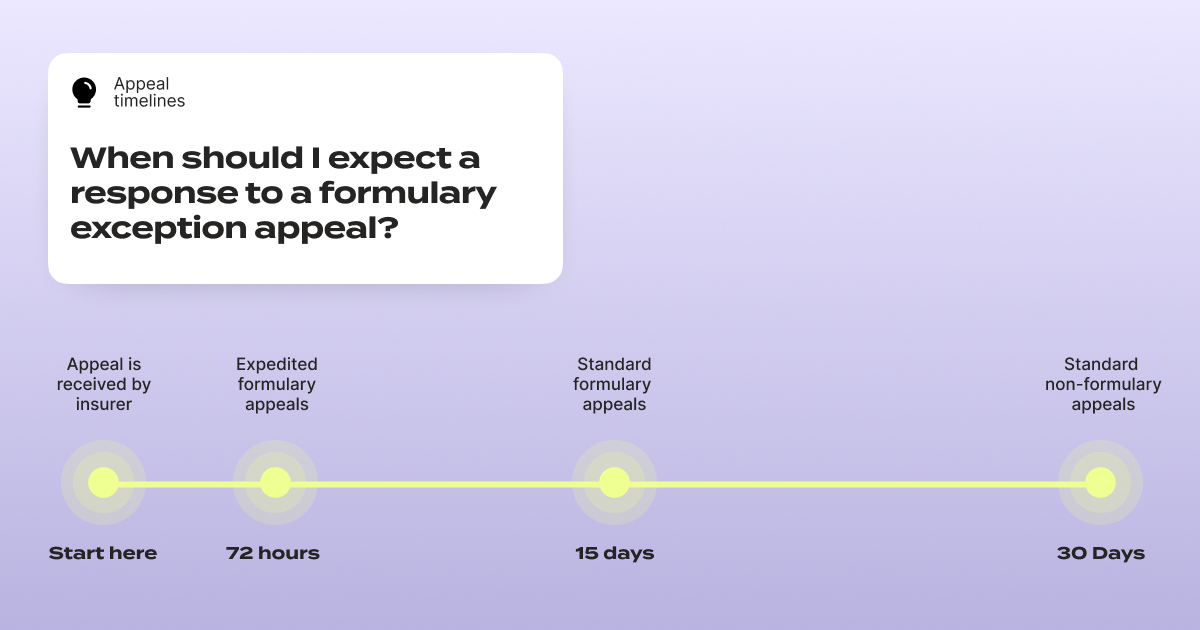

One critical timeline to know: under federal rules, insurers generally must provide expedited review within 72 hours for urgent requests and standard review within approximately 15 days for pre-service appeals – far faster than the standard 30-day review window for regular appeals.

But here's the catch: if you don't specifically request an expedited review and explain why your situation is urgent, many insurers will default to the standard timeline. If your health could seriously worsen by waiting, you have the right to request that 72-hour review. Put it in writing. At the very top of your appeal letter, write: EXPEDITED REVIEW REQUESTED (72 HOURS). Make sure it's impossible to miss.

Also double-check whether your insurer has a separate fax number or submission process for expedited appeals — they often do.

Know your rights, and state them clearly. Timelines vary by plan type, so always confirm your plan's specific rules.

Know Your Plan Type

Appeal rights and timelines can vary depending on your plan type and sponsor.

If you work for a large employer, you're likely on a self-funded plan, meaning your employer ultimately pays claims and serves as the plan fiduciary under the Employee Retirement Income Security Act (ERISA). In these cases, your appeal can reference your employer's duty to act in the best interests of employees.

Fully insured employer plans are generally subject to ERISA, the Affordable Care Act (ACA), and applicable state insurance regulations. Individual and exchange plans typically follow ACA and state rules. Federal and state employee plans, Medicare, and Medicaid each have their own appeal procedures and timelines.

Always review your plan documents — often called a Summary Plan Description (SPD), Evidence or Certificate of Coverage (EOC), plan brochure, or member handbook — to confirm the specific rules for formulary exceptions that apply to you.

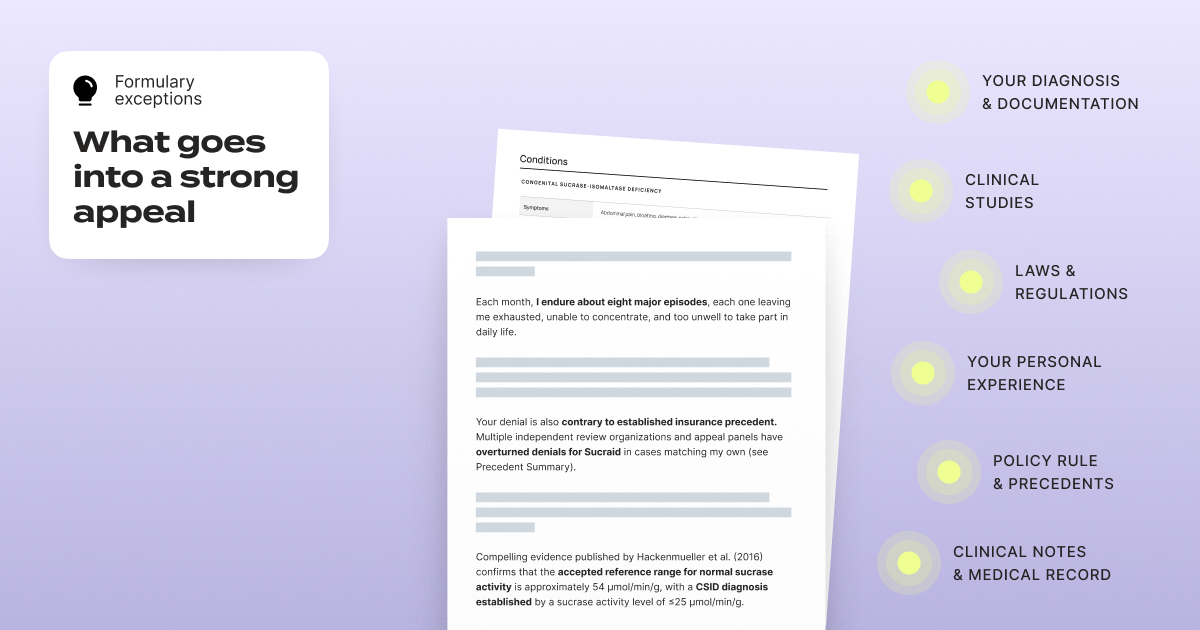

What to Include in Your Formulary Exception Letter

A request that says "I need this medication" isn't enough. The ones that succeed build a structured case with specific, documented evidence. Here's what your letter should include:

The letter itself

Subject line: Request for formulary exception / appeal of non-formulary denial for [Drug Name]

Identify the denial. Your name, member ID (on your insurance card), date of denial, and the medication you were denied.

State what you're requesting. Be explicit: "I am requesting a formulary exception for [drug name], and coverage at the medically necessary level." Use the words "formulary exception." Don't leave room for miscategorization.

Explain why you need this specific drug. This is the core of your case:

- Your diagnosis and its severity, supported by test results or doctor's notes

- Why this drug is appropriate for your condition, citing clinical studies that support its effectiveness

- Why alternatives failed or are unsafe – name each one, how long you tried it, and what happened. If any alternatives carry warnings or contraindications for your situation, state that clearly.

- If you're stable on the drug: explain the improvement you've experienced and why switching creates risk – relapse, ER visits, loss of function, need for additional treatments. Spell out the real-world consequences rather than keeping it abstract.

Add legal and policy support. Reference applicable laws and protections – many states have laws against non-medical switching, and federal protections may apply depending on your plan type. If you're currently taking the medication and losing coverage could cause a gap in care, note this clearly and mark your request as "URGENT: Expedited review requested" to invoke the 72-hour review timeline.

Close with your ask and a list of supporting documents included.

And if you need help putting all of this together – that's where Claimable comes in. You answer some questions about the denial, your medical history, and personal story, and we get to work researching all the right studies, laws, and other evidence you need to build a strong appeal. Then, we fax and mail it for you. Our job is to translate your experience into a lawyer-level appeal letter, and give you the best possible chance of getting that exception approved.

The supporting documents (include as many as you have)

- Your denial documentation (notice letter, denial letter, portal screenshot or app screenshot)

- A Letter of Medical Necessity or the Medical Exception Form from your doctor

- A clear list of previously tried alternatives (drug name, dates, outcome, side effects)

- Relevant clinical notes from your medical records

- Any clinical studies supporting your medication for your condition

- A copy of your plan's rules, called a Summary Plan Description (SPD), Evidence or Certificate of Coverage (EOC), plan brochure, or member handbook

Where to find your clinical documentation: Your provider's patient portal is your best starting point (e.g., My Chart). Look for:

- Your medication list – showing what you've tried and why you stopped each one

- Your allergy list – documenting adverse reactions to specific drugs

- Visit notes from appointments where you and your provider discussed treatment decisions

If you can't find what you need in your portal, ask your provider directly for the clinical notes that document your treatment history – specifically the notes showing why alternatives failed or aren't appropriate for you.

Getting the Letter of Medical Necessity: If your provider is busy (and they always are), send them a template and specific talking points (we have one available here). Follow up – a single email that goes unanswered isn't enough when your coverage is on the line.

Common Mistakes That Waste Time or Hurt Your Request

Trying to resolve things by phone. Calling to check on the status of your request? Good to do, and can actually help – insurers have been known to claim they never received something until you provide tracking details (and then suddenly, they find it!). But don't try to appeal or negotiate a coverage decision over the phone. You don't want a low-level phone representative making decisions about your care. You want a written record, a formal process, and a qualified reviewer examining your evidence. Get everything in writing, ask them to send documentation of anything you discuss over the phone, and confirm everything they tell you in writing.

Filing a complaint with the wrong regulator. Many patients spend weeks drafting a complaint to their state Department of Insurance – only to learn that their plan is regulated at the federal level, where the state DOI has no jurisdiction. The majority of employer-sponsored plans are governed by federal law (ERISA), not state law. Before you spend time on a regulatory complaint, verify who actually regulates your plan. Your denial letter should include this information, or you can call your insurer and ask specifically: "Who handles external appeals for my plan?"

Not asserting your timeline rights. As mentioned above, formulary exceptions have faster review requirements than standard appeals. If you don't explicitly cite these timelines in your request, insurers have little incentive to prioritize it.

If Your Formulary Is Changing, Here's How to Prepare

If you've received notice that your medication is being removed from the formulary on a future date, don't wait for that date to arrive to take action.

- Get the longest supply you can now. If you're eligible for a 90-day fill, request it before the change takes effect. This gives you a buffer while you work through the exception and appeal process.

- Request a continuity of care exception. You can request a continuity of care exception to maintain coverage while your appeal is pending. Whether it is granted depends on your plan's rules, but it is absolutely worth asking.

- Have your provider file a new prior authorization on the first day the change takes effect. Your existing PA is effectively expired on the date the formulary change goes into effect, even though it shouldn't be. Your provider may not automatically resubmit a PA — but they can. Just ask. Once that new PA is denied, you have an active, current denial to appeal.

- Prepare your documentation in advance. Gather your clinical records, research the clinical evidence for your medication (or use Claimable to do the heavy lifting for you), and draft your personal statement. You don't want to be scrambling after you've been denied – you want to be ready to file immediately.

Don't Wait for the Denial Letter: Start Taking Action Immediately

You don't need to wait for the formal denial letter in the mail to start building your case. As soon as you know there's a problem – whether it's an app notification, a call from your pharmacist, or your doctor telling you they're switching your medication – make two phone calls.

Call your provider's office. Tell them you've been denied and you plan to challenge it. Ask for copies of the clinical notes that support your need for this medication – your treatment history, documentation of failed alternatives, and any relevant test results. Ask them to send it as quickly as possible.

Call your insurer. Request all documentation used to make the decision. Your denial letter (when it arrives) will likely include language stating you can request this – but you have to ask. Request:

- Clinical review notes

- Internal medical policies applied to your case

- Guidelines, criteria, or standards they relied on

- The name, credentials, and specialty of the reviewer

- Documentation of any automated systems or algorithms involved in the decision

Also file a separate claim file request – a formal request for your complete case file. This can take up to 30 days to fulfill (and insurers often don't comply unless you follow up), so getting it started immediately is smart. Consider sending it as a standalone request rather than bundling it with your appeal, since it may go to a different department.

Submit Your Appeal and Follow Up

Where to send it

Start with your denial letter or portal notice – it usually lists the appeals address, fax number, or portal upload path. If you don't see it, call the member services number on your insurance card and ask: "Where do I submit a member/patient appeal for a non-formulary denial?"

Some plans allow you to submit appeals through your online portal, which gives you a digital confirmation. If you fax, save the transmission receipt. If you mail, use certified mail with tracking.

When to follow up

If your appeal was faxed and the situation is urgent, call the next day to confirm they received it. If they say they don't have it, provide your fax confirmation details – they often "find" it once you can prove it was sent.

If your appeal was mailed, allow two to four weeks for delivery and processing. Once tracking shows it's delivered, start calling to confirm it's been logged and assigned for review.

Keep a simple log of every interaction: date, time, who you spoke with, what they said, and any reference numbers. This paper trail matters if you need to escalate.

What to Do If Your Formulary Exception Is Denied

A denied formulary exception is not the end. Your appeal rights include multiple levels of review, each with stronger protections – you can (and should!) keep fighting.

Request a second internal appeal. Your first step is a second internal appeal where a different reviewer – one who wasn't involved in the original decision – examines your case. Take a look at why they denied the request, add any additional evidence to support your case, and resubmit your appeal with REQUEST FOR SECOND INTERNAL REVIEW right at the top.

Escalate to external review. If your internal appeal is denied, you have the right to an independent external review – a decision made by a reviewer completely outside your insurance company. This is one of the strongest patient protections in the system, and insurers are bound by external review decisions.

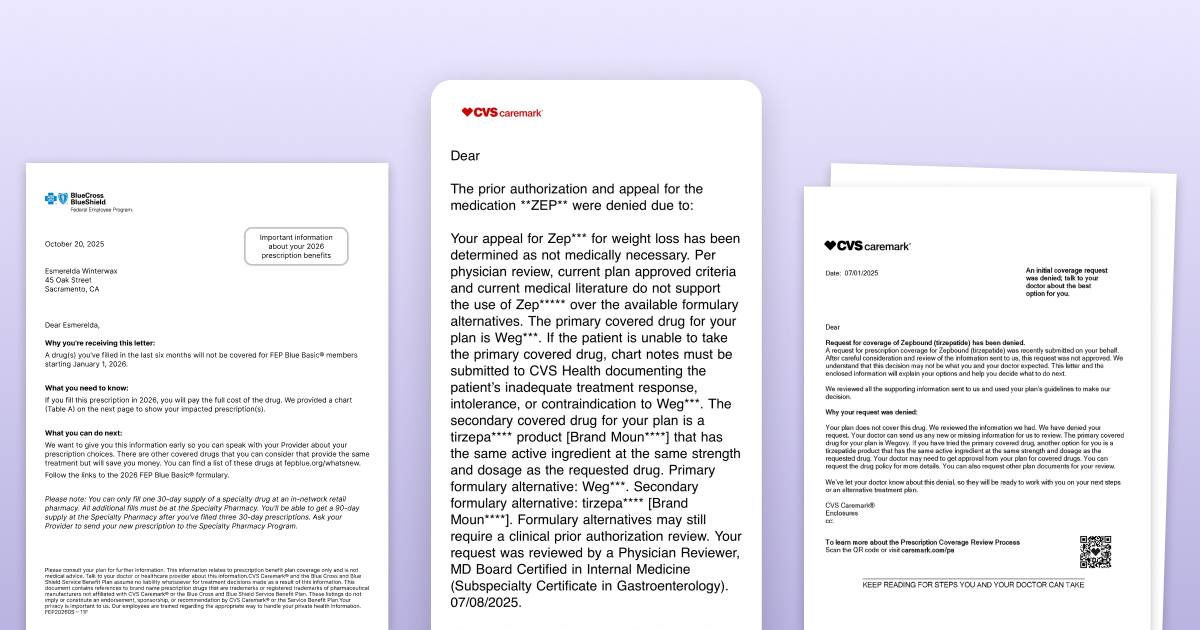

Real Examples: Formulary Changes Happening Right Now

CVS Caremark dropping Zepbound for Wegovy

CVS Health announced that starting July 2025, Caremark would prioritize Wegovy on its standard formularies and drop Zepbound – tied to a partnership with Wegovy's manufacturer, Novo Nordisk. Patients who were stable on Zepbound were suddenly told they'd need to switch, regardless of how well the medication was working for them.

If you're in this situation, the playbook is exactly what we've described above: secure an active denial (via new PA), then submit a patient appeal showing why the forced switch isn't appropriate for you – including your treatment history, failed alternatives, and the real-world consequences of switching.

BCBS FEP Dupixent Formulary Changes

In November, BCBS FEP Blue announced that Dupixent would no longer be on their formulary. Some FEP Blue plans use a closed formulary, meaning if Dupixent isn't on the list, you pay the full cost unless you win an exception. Dupixent is a popular drug used for a wide range of conditions like atopic dermatitis (eczema), nasal polyps, asthma and COPD, and many have been impacted by this coverage change – even those who were stable and responding well to treatment.

This isn't limited to FEP. BCBS Dupixent prior authorization requirements and formulary placement vary by state and plan – what's covered under BCBS Illinois Dupixent policies may differ from BCBS Alabama Dupixent coverage. If you've been denied, check your specific plan's formulary and denial reason before assuming another BCBS member's experience applies to you.

When the plan is this strict, your appeal packet needs to be especially tight: an active denial, a clear formulary exception request using the right language, a strong Letter of Medical Necessity, documented failure history, and – if you're stable on the drug – a clear argument for why forcing a switch is medically inappropriate. Especially for conditions like EoE, bullous pemphigoid, and prurigo nodularis, for which Dupixent is the only FDA-approved treatment, the argument for getting a formulary exception is clear and powerful.

How Claimable Can Help

If all of this seems like a lot, that's because it is. Insurers intentionally make the process tough to navigate, so you're more likely to just switch when facing a formulary change. But your treatment should be up to you and your doctor – not up to a rebate deal your insurer made.

We're here to help. Claimable builds customized, evidence-backed appeal letters that combine your personal health story with clinical research, policy analysis, and legal leverage – the three pillars that make appeals successful. This isn't a template or a generic form letter – every appeal is built specifically for your situation, your medication, and your insurer.

Claimable is free for many medications and situations, and otherwise costs just $39.95 + shipping. It's a fraction of the cost of a lawyer, and most cases resolve in under 10 days. We're here to help you navigate next steps. If you've hit a wall with a formulary denial, start your appeal here.

Frequently Asked Questions

Can insurance change my formulary mid-year?

Yes. While most formulary changes happen at the start of a new plan year, insurers can make changes mid-year – including removing drugs or moving them to higher tiers. These can happen at any time but are most common on 1/1 and 7/1. They're required to notify affected patients (typically 60 days in advance), but the notification process isn't always reliable. If you suspect a mid-year change, check your plan's current formulary directly on their website.

Can insurance change my formulary without notification?

They're required to notify you if you're currently on the affected medication. However, if you recently switched plans, changed your coverage level, or are newly prescribed the drug, you likely won't receive advance notice. The notification requirement only applies to patients the insurer already knows are filling that medication.

What is a formulary exception form?

Many formulary exception forms are designed for provider submissions – not patients. If you can't find a patient-specific form (which is common), you can submit a written appeal letter with the required information to your plan's appeals department. Plans are required to accept written appeals even without a standardized form. You can also use Claimable to generate and submit your request.

What is the difference between a formulary exception and a prior authorization?

A prior authorization (PA) is a coverage review required before certain medications will be approved — even if they're on the formulary. A formulary exception asks the plan to cover a drug that isn't on its approved drug list (or to override standard formulary rules). Depending on your situation, you may need to go through one or both processes — and they often happen in sequence, which is why they're easy to confuse.

How long does a formulary exception review take?

Federal rules generally require expedited review within 72 hours for urgent requests and standard review within about 15 days for pre-service appeals — often faster than the typical 30-day window for standard post-service appeals. However, timelines vary by plan type, so always confirm your plan's specific rules and explicitly request expedited review if your situation is urgent.

What if my provider says there's nothing they can do?

This is one of the most common – and most incorrect – things patients hear. Your provider may not be familiar with the formulary exception process or may assume that "not covered" means "not appealable." It doesn't. You have legal rights to challenge formulary decisions regardless of what your provider tells you. Consider sharing resources about the exception process with your provider, or explore your appeal options independently.

Do I need a lawyer to appeal a formulary exception denial?

No. While lawyers can help with complex cases, most formulary exception appeals can be handled effectively without one. What you need is the right evidence, the right language, and knowledge of your rights. Tools like Claimable are specifically designed to help patients build strong, evidence-backed appeals without the cost of legal representation.

Be the first to know

Get the latest updates on new tools, inspiring patient stories, expert appeal tips, and more—delivered to your inbox.

You're on the list!